Co-author David Pruitt

Davis v. Aethon Energy Operating LLC is more for lawyers than business people but it is worth noting. A Texas court of appeals affirmed a take-nothing judgment against lessors who sued over the lessee’s failure to provide required information on check stubs. The question asked of the jury did not match the requirements of the statute the lessor was suing under. The court measured the sufficiency of the evidence against the charge as given.

The Facts

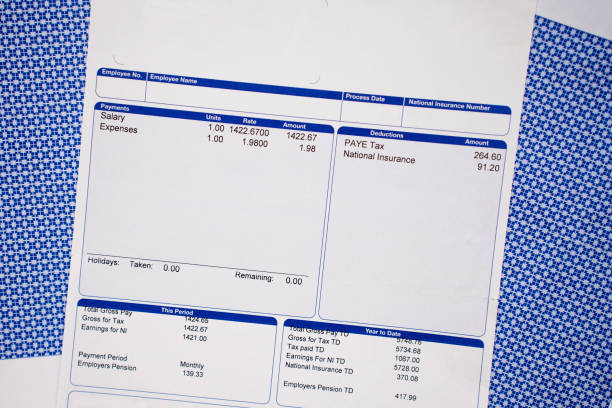

Lessors Lud and Charlotte Davis sued lessee Aethon and several related entities. The Davises’ leases required them to bear their portion of post-production costs, including a transportation fee that Aethon-related entity Scona charges for marketing gas.

During 2020, each check stub to the Davises listed the transportation charge as “$0.00.” The Davises suspected Aethon was embedding the fee in the total sales price and concealing the charge through its accounting methods. After an unsatisfying explanation from Aethon’s general counsel, the Davises concluded that Aethon was artificially inflating post-production costs. They sued in March 2021.

Also in that month, Aethon serendipitously changed its accounting practices and began separately itemizing the transportation fee, maintaining the change was unrelated to the lawsuit and was made in order to automate payout calculations for cost-free royalty owners.

The statute

Texas Natural Resources Code § 91.501 requires a payor to include information specified in § 91.502 “on the check stub, an attachment to the payment form, or another remittance advice that accompanies the payment.” Among the required disclosures are “any other deductions or adjustments.”

At trial the jury charge didn’t track the statute. Question Six asked whether Aethon failed to provide the Davises with the information “to which they were entitled each month” — not on “each check stub.” The court held that because no objection was made to the charge, the sufficiency of the evidence was measured by the charge as given, even if it is an incorrect statement of the law.

Under the language in the charge, the jury concluded that Aethon satisfied its statutory duty by disclosing the required information at some point in time other than on the check stub. Thus, an email from Aethon’s general counsel explaining the fee, combined with the fact that the fee was separately itemized beginning in March 2021, gave the Davises enough information from which to calculate the charge for the pre-March 2021 period, and allowed Aethon to satisfy its legal obligations as stated in the question. It probably helped Aethon that Lud Davis was a sophisticated royalty owner who had the information to calculate the fee at least two years before trial.

Bottom line – the jury charge

Questions to be answered by the jury are important. The Davises may have had a strong case under the text of § 91.502, but the jury evaluated the evidence against the question actually posed, not the as-written language of the statute. The evidence was legally and factually sufficient to support the jury’s verdict.